The Game Plan – Property Investment

29 March 2016

Property investment success is not dependent on your current income level or some sheer stroke of luck. It requires strategy. The post The Game Plan – Property Investment appeared first on Aspect Buyer's Agency.

Property investment success is not dependent on your current income level or some sheer stroke of luck. It requires the right strategy, mindset and the knowledge that building a successful property portfolio is not a get rich quick scheme. If you do property investment right, though, you can achieve financial freedom.

Let’s start with our investor profile. Here is a typical, young Australian couple. This may not be indicative of your personal situation, but it’s a good starting point to help you build your own game plan.

Own Home Value

$600,000

Debt

1 credit card of $5,000, paid monthly in full

2 car loans of $40,000 total, with monthly repayments of $820 @ 8.49% interest

Savings

$15,000 in savings and $200 saved weekly

Mortgage

$400,000 (average mortgage in NSW were at a record high of $544,000 in December 2015*)

Available Equity

$200,000

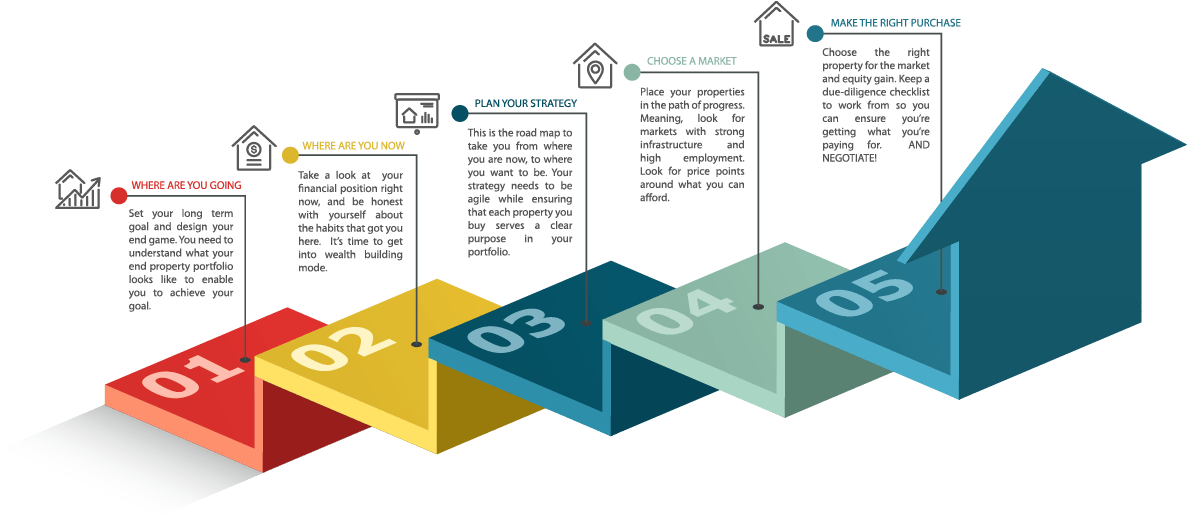

Here’s a quick overview of the 5-step process to take you from home owner to property investor extraordinaire.

Click on the image to expand.

1.Where are you going?

The very first thing to do when embarking on property investment is to set a long term, specific goal. It’s cool to say that you own 50 properties, but the number of properties you own is irrelevant. Your goal should be focused on the net value of your assets and the net rental yield you receive.

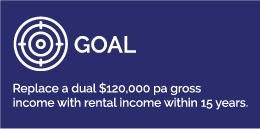

This is an example of a long term, specific goal.

Once you’ve set your goal, this should be the driving force behind every property purchase you make. The income may fluctuate, and of course the time span will reduce, but the end-game remains the same. Remember, it’s not about how many properties you need (or want). It’s about the result that your properties will generate for your portfolio.

2. Where are you now?

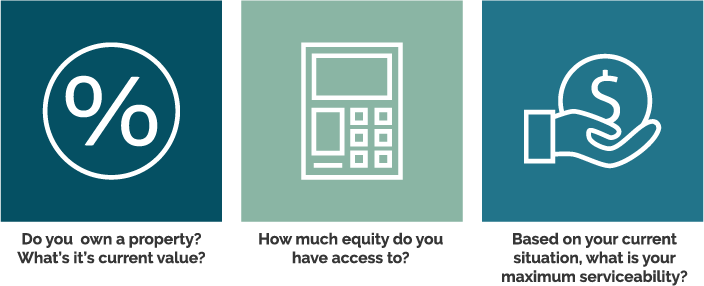

It’s really important to have a clear understanding of where you’re positioned right now, so you can set the right path to reach your end goal. The fundamentals of the game plan apply to everyone, but your situation is unique to you. Remember, the aim here is to form the foundations of a solid property portfolio that will allow you to achieve your goal. You need to understand how you’re sitting financially, so be prepared to seek the answers from those who can readily access the right data and give you sound guidance – your mortgage broker, financial planner or accountant should be able to help here. Let’s look at the factors that are critical in formulating your property investment strategy.

Your Assets

Your Financial Position.

Answer these questions to get a clear picture of your buying power.

- What are the banks willing to lend you?

- How much cash or equity will you need to satisfy your loan-to-value (LVR) ratio requirements on your investment property?

- What is the maximum amount of property you can buy based on the amount of cash and equity you currently have, and the LVR you expect to invest at?

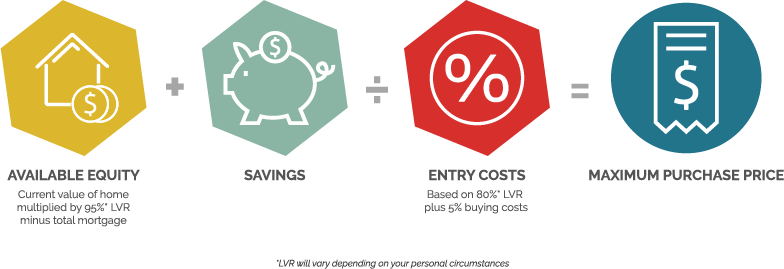

What’s your buying power?

Let’s do some quick sums.

Current value of your home (CVH) minus total mortgage (TM) equals total equity you have access to. (TE)

CVH – TM = TE

Based on our couple from our investor profile, this equates to:

$600,000 – $400,000 = $200,000

What we need to know, though, is the available equity (AE). So we need to factor in the 95% LVR over the family home.

$600,000 x 95% = $570,000 available equity

- Our couple has $200,000 in equity

- With an allowance of 95% LVR, releases $170,000 for further investment

- They already have $15,000 in savings

So, taking their $15,000 in savings, in addition to their available equity of $170,000, our couple now has $185,000 to put towards building their portfolio. With $185,000 in cash and equity and an 80% LVR, we can work out easily the maximum amount we can spend on entering the world of property investment. With a 20% deposit plus an additional 5% in buying costs, we can put total entry at 25%.

Maximum purchase price: $185,000 divided by 25% = $740,000

Do you have sound wealth building habits?

Many people fall into the trap of believing that if they work harder, they can earn more, and in turn build wealth. Generally, though, the more you earn, the more you spend. Good financial habits are really about how you manage your money. Not the money you might one day have, but the money you have now.

If you’re serious about investing in your future, you need to get business-minded about your finances. Just as a business will have budgets and cash flows, so too should your household. If you visit the app store and type in ‘budget planner’, you’ll get a whole list of free and simple apps that you can use on your smartphone.

Do you have a savings plan? If not, you need to get your hands on a copy of The Richest Man in Babylon . Written by George S. Caslon in 1926, this book is a classic in financial literature. It’s principles, written in parables and set in Ancient Babylon, are as relevant now as they ever were. The very first lesson in this book is “Start thy purse to fattening”. Quite simply, pay yourself first. Before you pay your bills, buy groceries or put fuel in your car, set aside at least one tenth of your income in savings. Most of us tend to save what’s left over after all our expenses. Flip this on its head, watch your savings account grow, and notice that you don’t even miss the money.

Making money is a mindset, an attitude, a willingness to do what it takes.

Get real with yourself about your financial habits. Read more on this here.

Do more with what you have.

Again, from The Richest Man in Babylon :

“Gold in a purse is gratifying to own and satisfieth a miserly soul but earns nothing.”

Always consider ways to make your money work harder for you. Property investment is a long-term strategy, but consider opportunities in front of you right now.

- Can you add value to your current property through a renovation?

- If your income is limited, are there other opportunities to earn?

- Can you afford to reduce debt more quickly?

Consider changes in circumstance.

Most of us tend to consider wealth building a compartment of our overall lives. It’s not. To be truly successful in building wealth, it needs to be integrated into every aspect of your life. So, it’s essential to consider how our lives evolve, and potential risks and stumbling blocks that may exist from a holistic perspective.

- Don’t put all your eggs in one basket. What buffers do you have in place for your personal life?

- What would happen if you stopped earning your current income tomorrow?

- Is your job secure?

- If you’re incapacitated, and can’t work, how do you get paid?

- Do you have a dual income? Is this sustainable?

- Is your family still growing?

- If you’re single, what happens to your income when you start your own family?

- Is your family healthy?

- What happens if you decide to make a tree or sea change?

Every decision we make in life has risk associated to it, so don’t be dissuaded. Just take a realistic look at your life, and put measures in place to ensure if any major changes do occur, you won’t take toO much of a financial hit.

3. Plan your strategy.

There are three distinct phases in investing.

Acquisition Phase

This is the most critical stage. Get it right, you build a solid foundation to allow you to move into the consolidation phase and eventually into gaining the financial freedom you desire in the lifestyle/legacy phase.

Consolidation Phase

In this phase you consolidate to reduce debt, lower your LVR and increase cash flow. That’s exciting!

Lifestyle/Legacy Phase

Once you make it here, you’ve achieved financial freedom. While your enjoying the spoils of your riches, keep a sharp eye on maintaining the financial freedom you’ve worked so hard to create. Essentially, this is the management phase.

Each property you purchase has to serve a purpose in your portfolio to move you successfully through these phases, remembering that financial freedom is the ultimate outcome.

Now that you understand the different phases of property investment, let’s take a look at the three different tactics that contribute to your overall property investment strategy.

Long-term asset accumulation and capital growth

These properties are in stable markets that see steady and continual growth over time.

Self-Supporting

These pretty much pay for themselves, and generate enough cash flow to support your servicing.

Acceleration Strategy

This approach is really about buying properties that generate short-term profits, which enable you to accelerate the growth of your portfolio. Implementing the acceleration strategy creates larger deposits for future property purchases, and and can help quickly reduce the debt on other long-term properties.

Note that the property type you consider contributes to your overall portfolio strategy. Don’t fall into the trap that many do, and take an accelerated approach to all property investments.

The purpose of your very first property really should be to create more equity for a deposit on your next property.

4. Choose your market.

This step is critical for first and second time investors. You don’t have to buy an investment property in the suburb or city that you live in. Unless the fundamentals of where you live actually align with your property investment strategy, it’s probably best to look at other locations. Capital city locations and major regional cities with strong infrastructure, industry and job security are good places to start. Seek out markets that offer this at the right price point.

5. Make the right purchase.

Now that you know the type of property you’re looking at and why, you can embark on the exciting part of finding the right property that serves your overall purpose. This is where a due-diligence checklist is vital, so you can take a systematic approach to selecting the best fit-for-purpose property for your portfolio.

- Research your potential markets and narrow it down to one or two options

- What type of property in the chosen market is in great demand by the local residents (house, unit, etc)

- Check if any maintenance work will be required in the short-term

There you have the five-step game plan to building a successful property portfolio. It can be pain-staking actually sitting down and running all these numbers, but it’s absolutely essential. This is your life, so be smart about it.

The second phase of your property investment strategy should be looking at future purchases and accumulating your next deposit. We’ll look at this in a future article. Now, if you haven’t done so already, create your investor profile and determine your long-term goal. Use our investor profile as a guide.

Happy investing!

Disclaimer:

The information on this website is general in nature and does not take into account your personal circumstances, financial needs or objectives. Before acting on any information, you should consider the appropriateness of it and the relevant product having regard to your objectives, financial situation and needs. In particular, you should seek independent financial advice from your accountant or financial planner.